Six Million Home Foreclosures: Are FDIC Insured Banks the Next Time Bomb? (Part 2)

http://seekingalpha.com/article/159368-six-million-home-foreclosures-are-fdic-insured-banks-the-next-time-bomb-part-2

_________

"Over a year ago Hank Paulson declared "The US Banking System Is A Safe and Sound One", the market's reaction to that piece of news was to short Fannie (FNM) and Freddie (FRE) into oblivion. A key issue there was holdings of mortgaged backed securities, specifically RMBS; valuations of those things depended on (a) their credit rating, (and once the LTV started to slip the rules said they had to be downgraded, so the price tanked), and (b) there was a rule of thumb that the value of those things was what an equivalent Treasury cost, less the cost of a CDS to insure them; when fear took over, the cost of a CDS went through the roof, the "market" (it never was a real market), froze. Then there was Lehman.

What drove that crisis was fear of the future, and the reason so much money was required to bail out the players ($2.7 trillion so far) was that previously if you had a "good credit score" you could borrow short-term Treasures, and buy an RMBS on 100% margin, and make a fortune; then the margins got called.

What happened was nothing different from a gambler going into a casino, borrowing from the house, using that money to bet on a "sure thing", and losing. Lucky for the gambler the "house" decided he was too big to fail - if you or I were to do something like that, we would be lucky to get away with a pair of broken legs.

Now the future is threatening to arrive:

There are two issues, (a) how much of that $2.7 trillion paid out mainly by the Fed (largely without any oversight by Congress) will get paid back, and (b) what's going to happen to the legacy banks who (then) had the luxury of being able to "take a view" on their portfolios of "originate and hold", and make a provision.

Right now the "reserves for losses" of FDIC insured banks is $211 billion on a portfolio of $7.625 trillion of loans and leases plus another $1.365 trillion of RMBS. In the circumstances that looks a tad light.

But the die is still rolling, and where it ends up will determine how much the "Too Big To Fail" card-sharks pay back, and how much of the $1.422 trillion of equity capital of the FDIC banks gets destroyed.

It's sometimes easy to forget that in this war the front line is foreclosures; although you wouldn't think that from the news. All you get is occasional pretty charts from the Mortgage Bankers Association with percentages (it's never quite clear of what), plus sound bites from the rating agencies like "the cure rate went down last month" or from RealtyTrac: "total filings went up last month".

From that trickle of managed, massaged and censored dispatches, it sounds suspiciously like somebody (or some-bodies), is trying to hide something.

Like a ticking bomb?

Perhaps the bottom in house prices was in May or perhaps there will be another leg down, but that's starting to be academic; a bottom is somewhere in the neighborhood. The story now is foreclosures; that's what drove house prices down to where they are now and that's what will keep them down. The acid on that cake and the nightmare for anyone in negative equity, is how many there will be by the time this is all over?

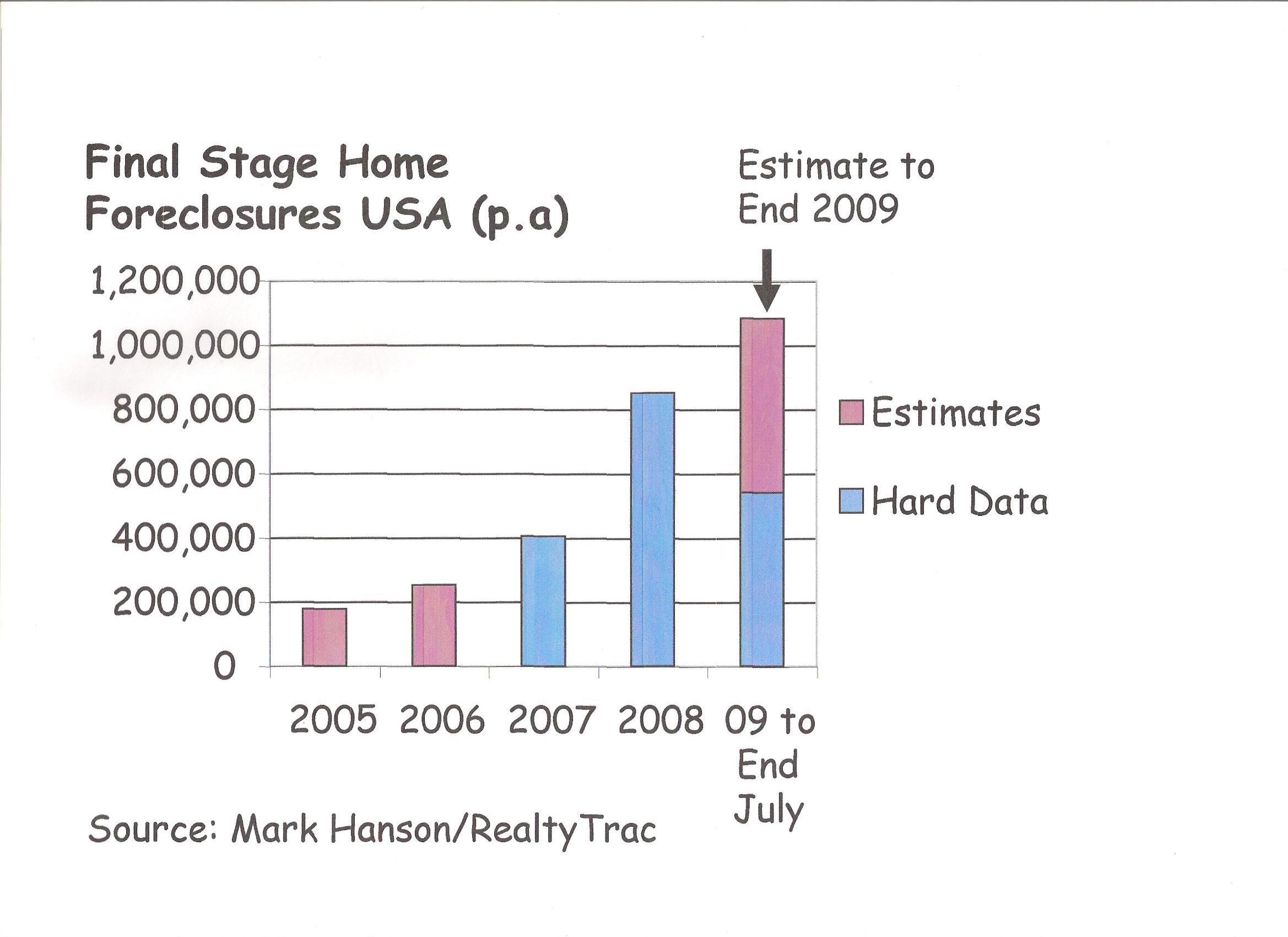

Since January 2005 over two million homes in USA have been foreclosed, that's about 1.7% of the total housing stock.

Many of those were family homes, so that's probably already directly affected about 3.5% of the American population.

This is the Bomb:

Right now in the USA there are over two million mortgages in either the first stage or the second stage of foreclosure; a large majority of those will end in foreclosure. At the current rate of "clearance" it will take two years for all of those to be processed.

And that's not counting new ones getting added to the pipeline at a rate of about 100,000 a month. That's clearly not something that anyone thought worth mentioning in the one hundred pages of turgid drivel "The Industry" shoveled out over the past three months; that I ploughed through to make sure I got it right (dear reader - just for you). And you wonder why there is a credit crunch?

The News Is, It Ain't Pretty

The headline data that is typically released, for example by RealtyTrac (i.e."360,000 Filings In July") is an aggregation that has to be disaggregated to make any sense of it, there are three stages:

The borrower can normally "cure" the process at any point, typically up to five days before the date of sale, although some mortgages give the lender the power to push through to disposal of the property as soon as the loan becomes delinquent. In most cases the process is non judicial and governed by the wording of the mortgage so there is no requirement to involve the Courts and the only option the borrower has to stop or delay the process is to pay up.

It's hard to get data, the best source I found was Mark Hanson plus there was data here and there from RealtyTrac. This is what I managed to cobble together:

That's not complete data, presumably that exists somewhere but it's not in the public domain. The reason there are more 1st Stage than 2nd Stage than Final Stage is (a) because some mortgages are cured (no hard data on how many) and (b) because the flow through from 1st to 2nd and Final is not linear.

An optimist might say that it looks like there is a top developing since Stage 1 and Final Stage are flattening; here are some theories:

Which?

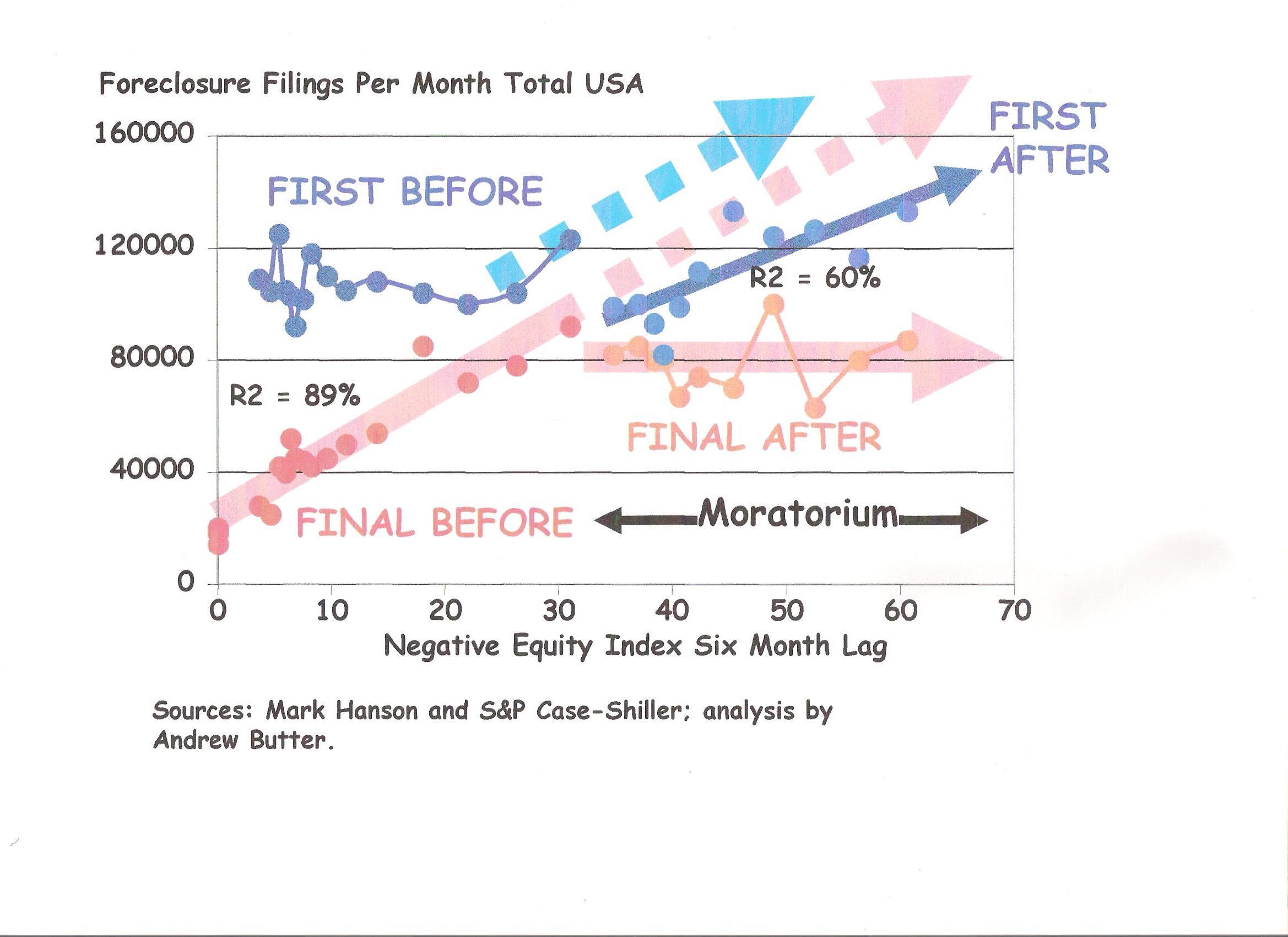

This is a plot of the difference between the S&P Case-Shiller 20 City Index and the final foreclosure number with a six-month lag, starting at the top where it was 207 (i.e. in January 2008 the Index was 181, so the difference is 26 and that's compared to foreclosures in June 2008 on the chart (six months later)). That's a measure of the Negative Equity of households.

This is the way I read that chart:

That appears to go against the theory that the moratorium encouraged or encourages people to default.

It's interesting how bankers, accountants and rating agencies never seem to miss an opportunity to blame their incompetence on the innate dishonesty, lack of personal ethics and downright crookedness of ordinary Americans, as if this whole thing was caused by Liar Loans, i.e. Liars. One of the turgid self-satisfied reports I read was about how the FBI "ought" to mobilize up to catch the people who "lied" as if that was what caused this disaster. Well I've met a lot of bankers, accountants and people from rating agencies, and I've also met a lot of ordinary Americans, and I don't think that I need to explain where my sympathies lie ( http://seekingalpha.com/article/157808-liar-loans-not-the-problem ) in that department. The track of the blue dots appears to prove my point.

It is likely also that easing off on foreclosures, was one, and perhaps the only reason for the recent "bounce" in the S&P Case-Shiller Index (helped perhaps by seasonal factors).

The Effect Of The Moratorium

The problem is that over the past nine months, despite the moratorium, another 1.2 million new 1st Stage Fillings were made, yet "only" 850,000 "left" the system to foreclosure, so that's another 350,000 in the system on top of the estimated 1,750,000 that were in the system in the first place (1st and 2nd Stage).

So that's 2,100,00 still "stuck" in the system, less the "cures", which are hard to gauge, I could not find consistent data on that.

Although if you have gone past the 1st Stage to once an auction date has been set (2nd Stage), the chances of modification or cure are much less; and from the first chart it is clear that the moratorium had little or no effect on the progression from 1st Stage to 2nd Stage. That suggests that unless new measures are brought in, the system might simply be playing catch up. "

August 2026 July 2026 June 2026 May 2026 April 2026 March 2026 February 2026 January 2026 December 2025 November 2025 October 2025 September 2025 August 2025 July 2025 June 2025 May 2025 April 2025 March 2025 February 2025 January 2025 December 2024 November 2024 October 2024 September 2024 August 2024 July 2024 June 2024 May 2024 April 2024 March 2024 February 2024 January 2024 December 2023 November 2023 October 2023 September 2023 August 2023 July 2023 June 2023 May 2023 April 2023 March 2023 February 2023 January 2023 December 2022 November 2022 October 2022 September 2022 August 2022 July 2022 June 2022 May 2022 April 2022 March 2022 February 2022 January 2022 December 2021 November 2021 October 2021 September 2021 August 2021 July 2021 June 2021 May 2021 April 2021 March 2021 February 2021 January 2021 December 2020 November 2020 October 2020 September 2020 August 2020 July 2020 June 2020 May 2020 April 2020 March 2020 February 2020 January 2020 December 2019 November 2019 October 2019 September 2019 August 2019 July 2019 June 2019 May 2019 April 2019 March 2019 February 2019 January 2019 December 2018 November 2018 October 2018 September 2018 August 2018 July 2018 June 2018 May 2018 April 2018 March 2018 February 2018 January 2018 December 2017 November 2017 October 2017 September 2017 August 2017 July 2017 June 2017 May 2017 April 2017 March 2017 February 2017 January 2017 December 2016 November 2016 January 2013 October 2011 September 2011 August 2011 July 2011 June 2011 May 2011 March 2011 January 2011 December 2010 October 2010 September 2010 August 2010 July 2010 June 2010 May 2010 April 2010 March 2010 February 2010 January 2010 December 2009 November 2009 October 2009 September 2009 August 2009 July 2009 June 2009 May 2009 April 2009 March 2009 February 2009 January 2009 December 2008 November 2008 October 2008 September 2008 August 2008 July 2008 June 2008 May 2008 April 2008 March 2008 February 2008 January 2008 December 2007 November 2007 October 2007 April 2007 March 2007 February 2007 January 2007 December 2006 November 2006 October 2006 September 2006 August 2006 July 2006 June 2006 May 2006 April 2006 March 2006 February 2006 January 2006 December 2005 November 2005 October 2005 September 2005 August 2005 July 2005 June 2005 March 2005 November 2004 October 2004